Saving for Your Child’s Future

Planning for a child’s future can feel like a big task, especially with so many options available. Whether your goal is to help with education, provide a financial head start, or build good money habits, starting early and staying consistent can make a meaningful difference over time.

Different accounts and investments can support different goals, from short-term needs to long-term growth. Even opening a small account and contributing regularly can be a meaningful first step.

Start Saving Early

Time is one of the most powerful tools for saving. Even small amounts set aside regularly can grow over the years through compound growth. Your money earns returns, and those returns begin earning returns as well.

Starting early also helps you spread contributions out over time, which can feel more manageable. Just as important, it creates an opportunity to build strong financial habits. When children grow up seeing money being saved regularly, they are more likely to carry those habits forward.

It is also helpful to keep inflation in mind. Over time, the cost of things like education tends to rise. Money that is not growing may lose purchasing power, which is one reason many families look beyond basic savings accounts for longer-term goals.

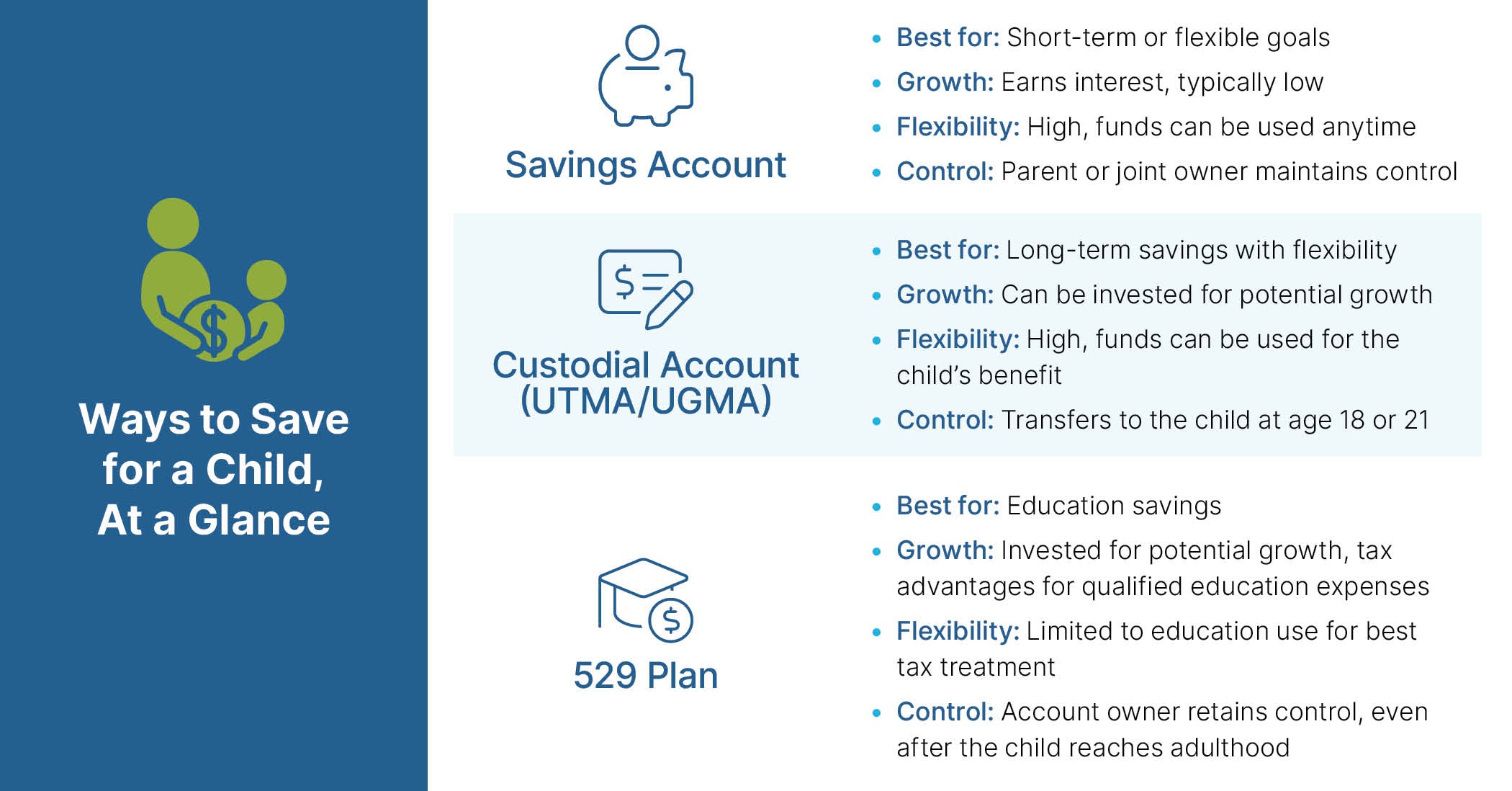

Savings Accounts for Children

Savings accounts are often used for short-term or flexible goals. They are easy to open, low risk, and allow funds to be accessed when needed. This makes them a practical place to hold money that may be used within a few years.

However, traditional savings accounts at large banks often pay very little interest. While rates can change, many accounts earn only a small amount over time. High-yield savings accounts typically offer better rates, but they are still designed for stability rather than long-term growth.

Savings accounts can also be a helpful teaching tool. As children get older, you can show them how deposits, withdrawals, and interest work in a real-world setting.

Custodial Accounts (UTMA/UGMA)

Custodial accounts, often called UTMA or UGMA accounts, are commonly used when families want to save or invest with flexibility in how the money can be used for the child’s benefit. An adult opens and manages the child's account, but the money legally belongs to the child once it is contributed.

The adult manages the account until the child reaches the age of majority, typically 18 or 21, depending on the state. At that point, the child takes full control and can use the funds for any purpose. This flexibility can be appealing, but it also means parents need to be comfortable with the child eventually making their own decisions about the money.

Investment Options for Long-Term Growth

For longer timeframes, many families consider investing to help savings grow over time. Investments can increase in value, but they can also go down, especially in the short term.

Some commonly used options include:

- Stocks: When you buy a stock, you are purchasing an ownership stake in a company. The value of that investment can rise or fall based on the company’s performance and market conditions. Stocks have the potential for higher long-term growth, but they can be more volatile, especially over shorter periods.

- Bonds: When you buy a bond, you are lending money to a government or company in exchange for interest payments and the return of your original investment at a set time. Bonds are generally considered more stable than stocks, though they may offer lower long-term growth.

- Mutual funds and ETFs: These pool money from many investors to invest in a mix of assets, such as stocks or bonds. This approach, called diversification, helps spread risk across many investments rather than relying on just one. These are often used for longer-term goals because they provide broad market exposure.

A simple way to think about which option to choose is to match your approach to your timeframe. Money that may be needed sooner is often kept in more stable options, while money that can stay invested longer may be positioned for growth.

A Note on 529 Plans

If saving for education is a priority, you may also hear about 529 plans. These accounts are designed to help families save for education expenses.

In general, contributions are invested, and the account can grow over time. Earnings are not taxed if the money is used for qualified education expenses, such as tuition and certain school-related costs. In addition, some states offer a state income tax deduction or credit for contributions, depending on where you live.

Because of these tax benefits, 529 plans are often used as part of a longer-term education savings strategy.

At the same time, these accounts are designed primarily for education, though recent rule changes have added more flexibility. For example, unused funds may now be rolled into a Roth IRA for the beneficiary, subject to certain limits. If funds are used for non-education purposes, taxes and penalties may still apply, so it’s helpful to plan ahead.

Making Saving a Habit

Consistency often matters more than the size of any single contribution. Building a routine around saving can make the process feel more manageable over time.

- Automate contributions: Setting up automatic transfers can help ensure money is saved regularly without needing to remember each time.

- Use gift money intentionally: Birthday or holiday money can be split between spending and saving.

- Involve your child: As they grow, include children in simple conversations about saving and goals.

These small steps can help turn saving into a long-term habit.

Choosing the Right Strategy

There is no single approach that works for every family. The right mix depends on your goals, timeframe, and how you want the money used.

For example, savings accounts are often used for shorter-term needs or when keeping money stable is the priority. Investments may be more appropriate for longer-term goals where there is time to ride out market ups and downs. Some accounts, like 529 plans, offer tax advantages for specific uses such as education, while others, like custodial accounts, offer more flexibility.

Because these decisions involve trade-offs among growth, flexibility, and control, some families choose to work with a financial professional to better understand how different options fit into their overall plan.

Bringing It All Together

Saving for a child’s future does not require a perfect plan or large upfront contributions. Starting early, staying consistent, and choosing options that align with your goals can go a long way.

Whether you begin with a simple savings account, explore custodial accounts, consider a 529 plan, or incorporate investments over time, each step helps build a foundation. Just as importantly, the process can help children learn about money in a practical way, setting them up with habits that can benefit them well into adulthood.